All Categories

Featured

Table of Contents

The are whole life insurance coverage and universal life insurance. The money worth is not added to the death advantage.

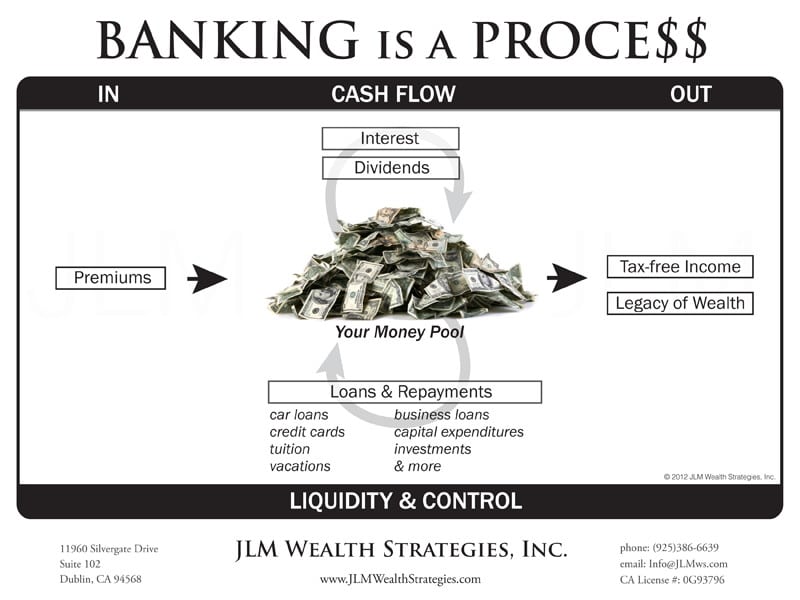

After one decade, the money worth has actually expanded to roughly $150,000. He obtains a tax-free finance of $50,000 to start a service with his sibling. The plan lending rates of interest is 6%. He pays back the funding over the following 5 years. Going this path, the rate of interest he pays goes back right into his plan's cash money worth as opposed to a financial establishment.

Bioshock Infinite Bank Of The Prophet Elevator

Nash was a money professional and follower of the Austrian school of economics, which promotes that the value of items aren't explicitly the result of conventional economic structures like supply and demand. Rather, people value cash and items in different ways based on their economic condition and demands.

One of the risks of typical banking, according to Nash, was high-interest prices on financings. A lot of individuals, himself included, obtained right into economic problem as a result of dependence on financial institutions. Long as financial institutions set the interest rates and car loan terms, individuals really did not have control over their very own wealth. Becoming your very own lender, Nash figured out, would certainly put you in control over your financial future.

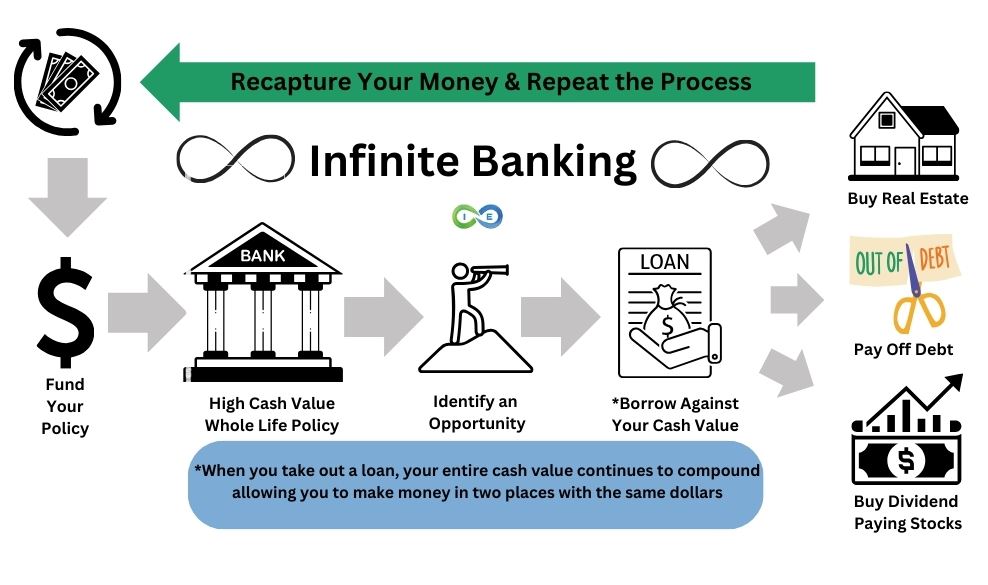

Infinite Financial needs you to possess your economic future. For ambitious people, it can be the most effective financial tool ever before. Right here are the advantages of Infinite Banking: Arguably the solitary most advantageous aspect of Infinite Banking is that it boosts your cash flow. You do not require to experience the hoops of a conventional bank to obtain a car loan; merely demand a policy financing from your life insurance policy firm and funds will be made offered to you.

Dividend-paying whole life insurance is really reduced threat and uses you, the insurance policy holder, a terrific bargain of control. The control that Infinite Banking uses can best be organized right into 2 categories: tax obligation advantages and possession defenses.

Can You Create Your Own Bank

When you use whole life insurance policy for Infinite Banking, you get in right into an exclusive contract between you and your insurer. This personal privacy supplies particular asset protections not found in other financial lorries. Although these defenses might differ from state to state, they can consist of protection from property searches and seizures, security from judgements and defense from lenders.

Whole life insurance policies are non-correlated assets. This is why they function so well as the financial structure of Infinite Financial. No matter of what takes place in the market (stock, actual estate, or otherwise), your insurance coverage policy keeps its worth.

Whole life insurance coverage is that 3rd container. Not only is the rate of return on your entire life insurance coverage policy ensured, your death advantage and costs are likewise ensured.

This framework lines up flawlessly with the concepts of the Perpetual Wealth Technique. Infinite Financial appeals to those seeking better monetary control. Below are its primary advantages: Liquidity and accessibility: Plan fundings offer instant access to funds without the limitations of standard financial institution loans. Tax obligation efficiency: The cash worth grows tax-deferred, and plan fundings are tax-free, making it a tax-efficient device for building wealth.

Infinite Bank Glitch Borderlands 2

Possession security: In several states, the cash worth of life insurance policy is secured from lenders, adding an added layer of economic security. While Infinite Financial has its advantages, it isn't a one-size-fits-all solution, and it features substantial downsides. Right here's why it may not be the most effective approach: Infinite Banking frequently calls for intricate policy structuring, which can puzzle insurance policy holders.

Imagine never ever needing to worry concerning small business loan or high rates of interest again. Suppose you could borrow money on your terms and develop wide range simultaneously? That's the power of unlimited banking life insurance coverage. By leveraging the cash worth of entire life insurance policy IUL plans, you can grow your riches and obtain money without counting on standard banks.

There's no set financing term, and you have the flexibility to choose the repayment schedule, which can be as leisurely as paying back the lending at the time of death. This versatility extends to the servicing of the car loans, where you can choose for interest-only repayments, maintaining the car loan balance flat and manageable.

Holding money in an IUL fixed account being credited rate of interest can commonly be much better than holding the money on down payment at a bank.: You've constantly desired for opening your very own pastry shop. You can borrow from your IUL plan to cover the initial expenditures of renting out an area, buying equipment, and working with team.

Infinite Bank Concept

Individual finances can be acquired from traditional financial institutions and debt unions. Obtaining cash on a credit report card is normally very costly with annual percent rates of rate of interest (APR) often reaching 20% to 30% or more a year.

The tax obligation treatment of plan financings can vary dramatically relying on your country of residence and the certain terms of your IUL plan. In some areas, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, plan car loans are normally tax-free, providing a substantial advantage. Nevertheless, in various other jurisdictions, there may be tax obligation implications to think about, such as possible taxes on the lending.

Term life insurance just offers a fatality benefit, without any cash value accumulation. This implies there's no cash money worth to borrow versus.

However, for car loan officers, the considerable guidelines imposed by the CFPB can be viewed as cumbersome and limiting. Finance police officers typically suggest that the CFPB's regulations develop unneeded red tape, leading to more paperwork and slower financing handling. Regulations like the TILA-RESPA Integrated Disclosure (TRID) rule and the Ability-to-Repay (ATR) needs, while focused on safeguarding consumers, can bring about delays in closing offers and boosted functional costs.

{kind=link}

Latest Posts

Whole Life Infinite Banking

Becoming Your Own Banker And Farming Without The Bank

Bank On Yourself Complaints