All Categories

Featured

Table of Contents

For the majority of people, the biggest issue with the boundless financial idea is that first hit to early liquidity triggered by the prices. Although this disadvantage of infinite financial can be minimized significantly with proper policy layout, the first years will always be the most awful years with any kind of Whole Life plan.

That claimed, there are certain limitless financial life insurance coverage policies created mainly for high very early cash money worth (HECV) of over 90% in the initial year. Nonetheless, the long-term efficiency will certainly typically substantially lag the best-performing Infinite Banking life insurance policies. Having access to that additional 4 numbers in the very first couple of years might come at the expense of 6-figures in the future.

You actually obtain some significant long-lasting advantages that aid you recoup these early prices and after that some. We locate that this hindered early liquidity trouble with boundless banking is much more mental than anything else as soon as completely discovered. If they definitely required every dime of the money missing from their limitless financial life insurance coverage policy in the first couple of years.

Tag: infinite financial concept In this episode, I talk about finances with Mary Jo Irmen that teaches the Infinite Banking Concept. With the rise of TikTok as an information-sharing system, monetary guidance and methods have actually located an unique means of spreading. One such strategy that has been making the rounds is the infinite banking concept, or IBC for brief, amassing endorsements from celebrities like rapper Waka Flocka Flame.

Within these policies, the cash money worth expands based on a rate set by the insurance firm. As soon as a considerable money worth builds up, insurance holders can get a cash worth loan. These car loans vary from standard ones, with life insurance coverage working as security, implying one can lose their insurance coverage if loaning excessively without sufficient cash money value to sustain the insurance coverage prices.

And while the attraction of these plans is noticeable, there are inherent restrictions and threats, requiring diligent cash value surveillance. The strategy's legitimacy isn't black and white. For high-net-worth people or business owners, especially those making use of strategies like company-owned life insurance (COLI), the advantages of tax obligation breaks and compound growth might be appealing.

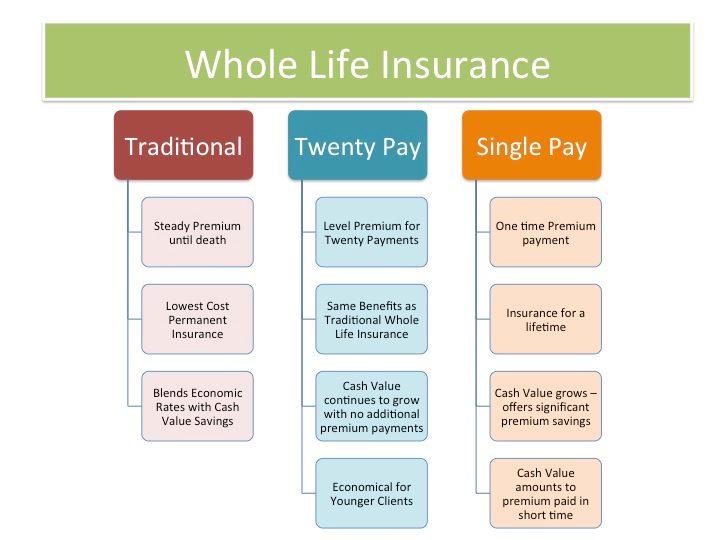

Become Your Own Banker Whole Life Insurance

The attraction of infinite financial does not negate its obstacles: Cost: The foundational demand, a permanent life insurance plan, is pricier than its term equivalents. Qualification: Not everybody certifies for whole life insurance policy because of strenuous underwriting procedures that can exclude those with certain wellness or way of life conditions. Intricacy and risk: The intricate nature of IBC, paired with its risks, might hinder several, specifically when simpler and much less high-risk options are offered.

Alloting around 10% of your regular monthly earnings to the plan is just not possible for many individuals. Component of what you review below is merely a reiteration of what has already been claimed above.

Before you obtain on your own into a circumstance you're not prepared for, understand the adhering to initially: Although the idea is commonly marketed as such, you're not really taking a loan from on your own. If that were the instance, you would not need to repay it. Instead, you're borrowing from the insurer and have to repay it with interest.

Some social media posts suggest making use of cash money worth from entire life insurance to pay for credit history card debt. The idea is that when you repay the financing with passion, the quantity will be sent out back to your investments. That's not just how it functions. When you pay back the funding, a portion of that rate of interest goes to the insurance policy business.

For the initial a number of years, you'll be paying off the commission. This makes it extremely hard for your policy to build up value during this time. Unless you can pay for to pay a couple of to numerous hundred bucks for the next years or more, IBC will not work for you.

Is Bank On Yourself Legitimate

Not everyone needs to depend exclusively on themselves for monetary security. If you need life insurance, right here are some useful tips to take into consideration: Consider term life insurance policy. These policies offer insurance coverage throughout years with considerable financial responsibilities, like mortgages, pupil car loans, or when caring for kids. Ensure to search for the best rate.

Copyright (c) 2023, Intercom, Inc. () with Scheduled Font Call "Montserrat". Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Reserved Font Call "Montserrat".

Infinite Bank

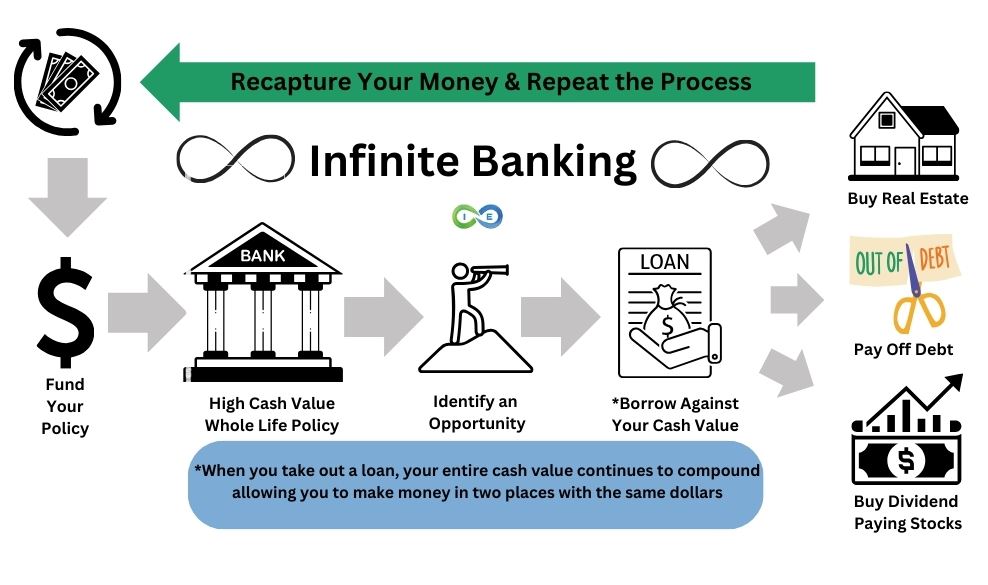

As a CPA focusing on property investing, I have actually combed shoulders with the "Infinite Banking Principle" (IBC) extra times than I can count. I've also talked to professionals on the topic. The main draw, other than the obvious life insurance coverage advantages, was always the concept of constructing up cash money value within a long-term life insurance policy plan and borrowing against it.

Sure, that makes good sense. But honestly, I constantly thought that money would be better invested straight on investments as opposed to channeling it with a life insurance policy policy Up until I uncovered just how IBC can be incorporated with an Irrevocable Life Insurance Trust Fund (ILIT) to produce generational wide range. Allow's begin with the fundamentals.

Infinite Banking Spreadsheets

When you borrow versus your plan's money worth, there's no set payment timetable, giving you the liberty to manage the finance on your terms. The cash value continues to grow based on the plan's assurances and returns. This setup enables you to gain access to liquidity without interrupting the long-term growth of your policy, gave that the car loan and passion are handled wisely.

As grandchildren are born and grow up, the ILIT can purchase life insurance policy plans on their lives. Family members can take loans from the ILIT, using the money worth of the policies to money investments, begin businesses, or cover significant expenditures.

A crucial facet of managing this Household Bank is making use of the HEMS standard, which means "Health, Education, Maintenance, or Support." This standard is typically consisted of in trust fund arrangements to direct the trustee on exactly how they can distribute funds to beneficiaries. By adhering to the HEMS standard, the depend on guarantees that circulations are produced necessary needs and lasting support, protecting the count on's assets while still offering member of the family.

Increased Flexibility: Unlike inflexible small business loan, you control the payment terms when borrowing from your own plan. This permits you to structure settlements in a way that aligns with your organization money flow. cut bank schools infinite campus. Better Money Flow: By funding business expenditures with plan car loans, you can possibly free up money that would certainly otherwise be locked up in traditional funding payments or equipment leases

He has the exact same equipment, but has actually also built additional money worth in his plan and got tax obligation advantages. Plus, he now has $50,000 offered in his policy to make use of for future possibilities or expenses., it's essential to see it as more than just life insurance coverage.

Rbc Infinite Visa Private Banking

It's concerning creating an adaptable funding system that offers you control and supplies numerous advantages. When utilized purposefully, it can enhance other financial investments and company strategies. If you're captivated by the capacity of the Infinite Financial Principle for your service, right here are some actions to think about: Educate Yourself: Dive much deeper into the principle with respectable publications, workshops, or examinations with experienced experts.

{kind=link}

Latest Posts

Whole Life Infinite Banking

Becoming Your Own Banker And Farming Without The Bank

Bank On Yourself Complaints