All Categories

Featured

Table of Contents

The are whole life insurance policy and global life insurance. The money value is not added to the death advantage.

The policy financing interest rate is 6%. Going this route, the interest he pays goes back right into his plan's cash worth instead of an economic organization.

Infinite Banking Toolkit

Nash was a money professional and fan of the Austrian school of business economics, which promotes that the value of goods aren't clearly the outcome of standard financial frameworks like supply and demand. Rather, people value cash and goods in a different way based on their economic status and needs.

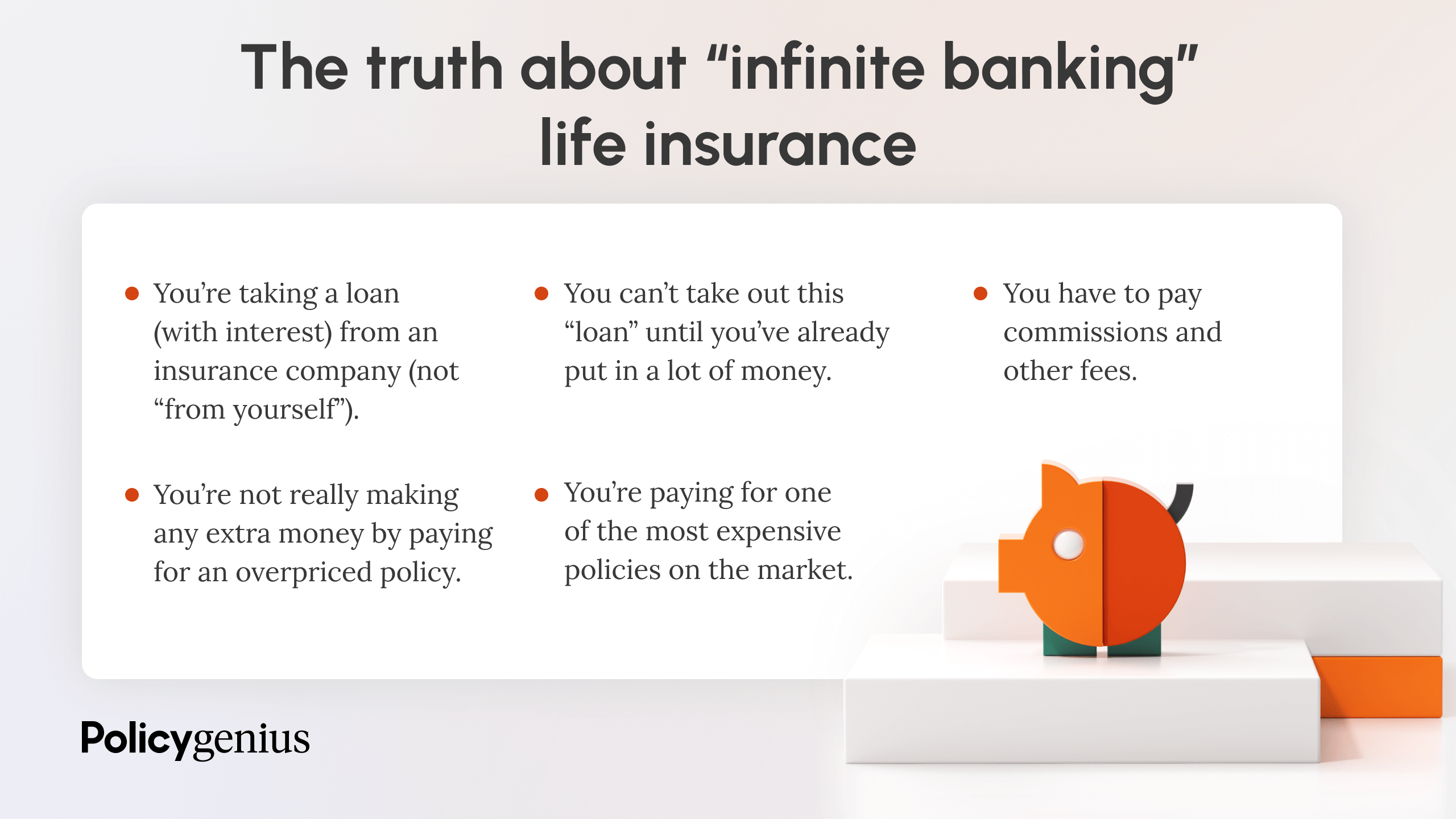

Among the pitfalls of traditional financial, according to Nash, was high-interest prices on lendings. Way too many individuals, himself consisted of, obtained into monetary problem as a result of dependence on banking organizations. Long as financial institutions established the rate of interest rates and loan terms, people didn't have control over their very own wealth. Becoming your very own lender, Nash identified, would put you in control over your economic future.

Infinite Financial needs you to own your economic future. For goal-oriented people, it can be the most effective monetary device ever. Below are the benefits of Infinite Banking: Perhaps the solitary most advantageous facet of Infinite Financial is that it improves your capital. You do not require to go via the hoops of a conventional bank to obtain a financing; merely demand a plan car loan from your life insurance policy business and funds will certainly be provided to you.

Dividend-paying whole life insurance policy is extremely reduced threat and provides you, the insurance policy holder, a good deal of control. The control that Infinite Financial supplies can best be grouped right into 2 classifications: tax obligation benefits and property securities - infinite financial. Among the reasons entire life insurance policy is suitable for Infinite Banking is exactly how it's taxed.

Infinite Banking Concept Canada

When you use entire life insurance policy for Infinite Financial, you enter right into an exclusive agreement in between you and your insurance coverage company. These securities might vary from state to state, they can include defense from possession searches and seizures, defense from judgements and defense from financial institutions.

Entire life insurance coverage policies are non-correlated possessions. This is why they function so well as the economic foundation of Infinite Financial. Despite what happens on the market (stock, realty, or otherwise), your insurance plan preserves its worth. Way too many individuals are missing this vital volatility buffer that assists secure and grow riches, instead dividing their cash right into two pails: checking account and investments.

Whole life insurance coverage is that 3rd container. Not just is the price of return on your entire life insurance coverage plan guaranteed, your death advantage and premiums are also assured.

Here are its primary advantages: Liquidity and ease of access: Policy loans provide immediate access to funds without the restrictions of conventional financial institution lendings. Tax performance: The money value grows tax-deferred, and policy lendings are tax-free, making it a tax-efficient device for building riches.

Infinite Banking Insurance Policy

Possession defense: In several states, the cash value of life insurance coverage is protected from lenders, adding an added layer of economic protection. While Infinite Banking has its qualities, it isn't a one-size-fits-all option, and it includes considerable disadvantages. Here's why it might not be the very best method: Infinite Banking commonly requires elaborate plan structuring, which can puzzle insurance holders.

Think of never having to worry concerning financial institution finances or high rate of interest prices again. That's the power of boundless financial life insurance coverage.

There's no collection loan term, and you have the freedom to select the repayment timetable, which can be as leisurely as settling the lending at the time of death. This adaptability encompasses the servicing of the lendings, where you can choose interest-only settlements, keeping the funding balance flat and manageable.

Holding cash in an IUL dealt with account being attributed passion can typically be far better than holding the cash on down payment at a bank.: You have actually always desired for opening your very own bakery. You can obtain from your IUL policy to cover the first expenses of renting out a room, purchasing tools, and hiring team.

Infinite Banking Institute

Individual lendings can be gotten from standard financial institutions and credit rating unions. Here are some key points to think about. Charge card can supply a versatile method to obtain cash for extremely short-term periods. Nonetheless, borrowing money on a bank card is usually very expensive with interest rate of rate of interest (APR) commonly reaching 20% to 30% or even more a year.

The tax treatment of policy loans can differ substantially depending on your country of house and the specific terms of your IUL plan. In some areas, such as North America, the United Arab Emirates, and Saudi Arabia, policy car loans are normally tax-free, using a significant benefit. However, in other jurisdictions, there may be tax implications to think about, such as possible taxes on the loan.

Term life insurance coverage only provides a survivor benefit, without any kind of cash money value accumulation. This suggests there's no cash value to borrow against. This short article is authored by Carlton Crabbe, Ceo of Resources for Life, a specialist in offering indexed global life insurance policy accounts. The information supplied in this article is for academic and informational functions only and ought to not be taken as financial or investment recommendations.

However, for loan police officers, the substantial policies enforced by the CFPB can be viewed as difficult and restrictive. Car loan policemans usually say that the CFPB's regulations produce unneeded red tape, leading to even more documentation and slower car loan processing. Regulations like the TILA-RESPA Integrated Disclosure (TRID) regulation and the Ability-to-Repay (ATR) needs, while intended at securing consumers, can result in delays in closing offers and raised functional prices.

{kind=link}

Latest Posts

Whole Life Infinite Banking

Becoming Your Own Banker And Farming Without The Bank

Bank On Yourself Complaints